04 Sep What Capital Position is Right for You? – Part III

BROOKE CIANFICHI, CHIEF OPERATING OFFICER

Part 3 – Why we choose to make Preferred Equity Investments[1]

This post will detail important factors to considers before investing with a Regional Center that will be placing your money in either the debt or Preferred Equity positions with the EB-5 Intermediary Company for a specific project.

Let’s discuss each level of the capital stack as it relates to you, the limited partner.

“Loan Model”:

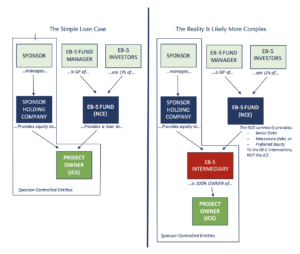

You are an EB-5 Investor, and your Limited Partnership Interest is placed in a NCE that makes a Senior Loan or a Mezzanine Loan to an Intermediary Entity that then places the money into a JCE.

The “Loan Model” was born out of two perceived benefits of a loan structure:

- Defined Term Length: Before certain countries were affected by long wait times (China), the green card process was approximately 5-years. A loan between the NCE and JCE (before the EB-5 Intermediary Entity was created) could be created with a set term of 5 years, providing an exit strategy, albeit very little return.

- Appearance of Collateral:The NCE could secure its loan with the asset owned by the JCE (a Senior Loan), or the NCE could secure its loan with ownership interests in the JCE (a Mezzanine Loan). Note that in both cases the EB-5 Investor isnot a direct beneficiary of the collateral, because the EB-5 investor is a Limited Partner in the NCE and the collateral was structured for the benefit of the NCE.

As deal complexity increased, Bank Construction Lenders began to express concern about an NCE making a loan directly to the JCE, or project level. Bank Construction Lenders want to provide the only Senior Loan at the project level and prohibit their borrower, the JCE, from incurring any additional debt. To legally accomplish this, sophisticated developers and their attorneys created an intermediary entity to acts a parent entity to the JCE, (the EB-5 Intermediary), which makes an equity contribution to the JCE rather than a Loan.

This new structure is illustrated in “The reality is much more complex”, below.

With the creation of this new EB-5 Intermediary, banks now typically require what is called an “inter-creditor agreement” and may require subordination of the Loan made by the NCE to the EB-5 Intermediary.

The structural considerations of a “Loan Model” today include:

(1) You are a few levels removed from the collateral: The loan to the EB-5 Intermediary is from the NCE of which you are a limited partner. As a limited partner in a debt fund with an EB-5 Intermediary Entity in place, you are not a lender with a direct Senior Loan or Mezzanine Loan to the project-level entity.

(2) You are subject to inter-creditor agreements: If your NCE has provided a loan to the EB-5 Intermediary, the lender who has the senior loan to the project will most likely require the NCE to sign an agreement that restricts the NCE’s rights. In the agreement, the NCE will (a) affirm that it is restricted in its ability to litigate or make claims against the collateral, (b) affirm that the NCE is restricted in foreclosing unless certain conditions are met by the NCE, (c) affirm that interest and principal payments can be restricted.

- You are subordinate to the JCE creditors:The JCE creditors come first; the collateral position of the NCE is subordinated and thus, in bankruptcy or liquidation the NCE must wait until the JCE creditors are repaid in full.

Other Considerations:

- When you are a limited partner in a “Loan Model” EB-5 investment, you may receive regularly scheduled interest-like payments generated from the underlying loan and the underlying loan has a scheduled maturity of typically 5 years, but it may include extension options.

- As a “Loan Model” EB-5 investor, you should consider the level of equity behind the total debt, with at least 25% equity expected.

- In the now special case where the NCE is the first mortgage lender, such as “The simple loan case”, you also should be asking why a bank first mortgage lender is not in place, as a first mortgage lender adds another layer of credit scrutiny to a project; not only did the developer have to prove to the equity investors that this was a sound project but he or she also had to prove to a heavily regulated bank that this was a sound project. (assuming a well-known bank governed by the Federal Reserve System is the lender)

“Equity Model”:

You are an EB-5 Investor, and your Limited Partnership Interest is placed in a NCE that makes a Preferred Equity Investment into an Intermediary Entity that then places the money into a JCE.

The major considerations of a Preferred Equity investor are:

(1) The returns act like debt returns: Preferred Equity is often structured with a potential “maturity date” (in quotes, because the return of principal cannot be guaranteed) as well as with preferred return distributions, allowing the Preferred Equity to behave like a debt security.

- Equity claims are subordinate to the debt claims in the capital stack:Traditionally speaking, the Preferred Equity investors are behind the Senior and Mezzanine investors in repayment. Given the subordination of the Senior and Mezzanine investors discussed above to the bank financing, as well as inter-creditor agreements ability to limit the rights of the debt at the NCE level, this issue is not as pronounced as it once was.

Though Preferred Equity investors may be at a disadvantage from the collateral viewpoint, there are many other factors to consider when deciding on your position in the capital stack. First and foremost is an understanding that investor in a Loan Model may not have as a clear a path to the collateral as they may be led to believe. The Preferred Equity investor in a project like the one from our initial case study would have many positives in his selected project that go beyond the collateral discussion: a strong first mortgage lender identified, and an experienced developer, with the assumption that there is strong equity behind the Preferred Equity position, such as 15-25% common equity.

In other words, identifying a project that has a lower likelihood of default is far more critical than choosing a project based upon the remedy in the event of a default.

AscendAmerica’s Position:

AscendAmerica considers the position within the capital stack that makes most sense for our unique and sophisticated investor, as based on all appropriate financial, experiential, and reputational considerations, because we are here to be the voice of the discerning investor. Our offerings are structured as Preferred Equity positions because that is the position within a capital stack that makes sense given the complexity and opaqueness of the “Loan Model” structures in today’s market. Finally, we choose and structure our offerings to reduce the chance that a default will ever occur.

Coming soon: Questions that Regional Centers do not want you to ask, but that you always should ask before making an investment!

[1]The information included in this blog post is for informational purposes only and not for the purpose of providing legal advice. You should contact your attorney to obtain advice with respect to any particular issue or problem. This is neither an offer to sell nor a solicitation of an offer to buy any security, which can be made only by the Confidential Private Placement Memorandum and all exhibits, attachments and supplements thereto and sold only by participating broker-dealers who are licensed to do so. Nothing contained in this article constitutes legal, investment, tax or other advice, and you should not rely upon it in making an investment or other decision. The opinions expressed herein or throughout this website are the opinions of the individual author and may not reflect the opinions of AscendAmerica or any of its officers, directors or employees.